Meta Description: How much does it cost to provide retail employee benefits? 2026 BLS data on health insurance, paid leave, and legally required benefits — all broken down for store owners.

When most retail store owners think about labor costs, they think about hourly wages. But the actual cost of employing a retail worker runs meaningfully higher than the rate on the time clock — and for many small and mid-size retailers, the gap comes as a surprise when they first dig into the numbers.

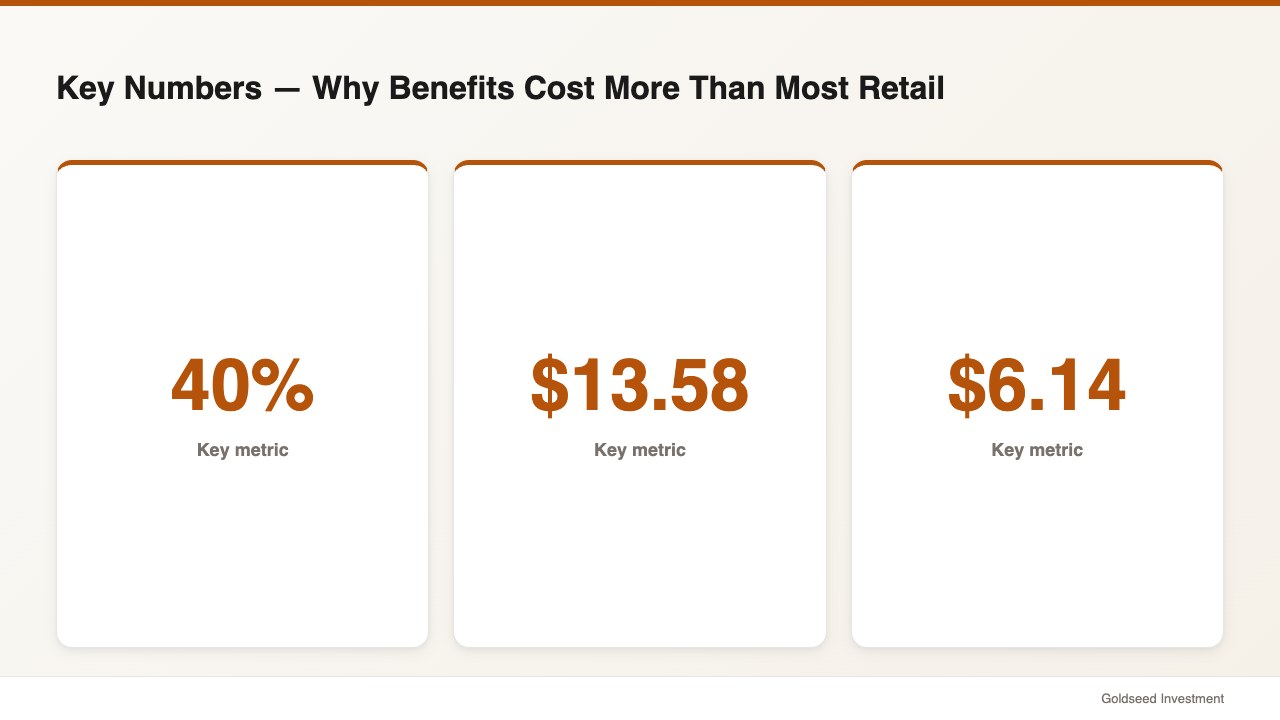

According to the most recent data from the U.S. Bureau of Labor Statistics, retail trade employers paid an average of $6.14 per hour in benefits for every worker in late 2025 — on top of average wages of $20.27 per hour. That brings total average compensation to $26.41 per hour, meaning benefits add roughly 30 cents to every dollar of wages paid in the retail sector.

For a full-time employee working a standard 2,080-hour year, that translates to approximately $12,771 in annual benefits cost before paying a single dollar of base salary. Understanding where that money goes — and how to benchmark it against industry norms — is foundational to running a financially sound retail operation.

This guide breaks down the employee benefits breakdown retail operators need, using the latest BLS data, and gives store owners a practical framework for calculating total labor costs in their own operations. For related context on overtime costs, see retail store operating costs breakdown. To see how payroll tools help manage total labor expense, see retail management software worth the cost.

Why Benefits Cost More Than Most Retail Owners Expect

There’s a persistent misconception among first-time retail employers: the cost of hiring someone equals their hourly wage plus a little for taxes. Once you factor in every required and voluntary benefit, the true employee benefits cost percentage payroll typically runs 25–40% higher than base wages alone, according to analysis from benefits consulting firms tracking mid-market employers.

Part of the surprise comes from how benefits are categorized. Some costs — like the employer’s share of Social Security and Medicare — are legally mandated and feel invisible because they flow through payroll automatically. Others, like health insurance or paid vacation, are more visible line items but difficult to estimate accurately when a business first offers them.

There’s also a difference between what retail employers offer versus other industries. Retail has historically been toward the lower end of the benefits spectrum compared to sectors like finance, technology, or healthcare. The BLS data confirms this: while private industry workers average $13.58 per hour in benefits (as of June 2025), retail workers receive $6.14 per hour — about 45% of the all-industry average. That gap largely reflects lower rates of health insurance and retirement benefit uptake in retail, particularly for part-time workers.

What this means for retail operators is that your retail benefits package cost looks different from what HR benchmarking reports designed for corporate employers suggest. You need retail-specific data — and that’s exactly what this breakdown provides.

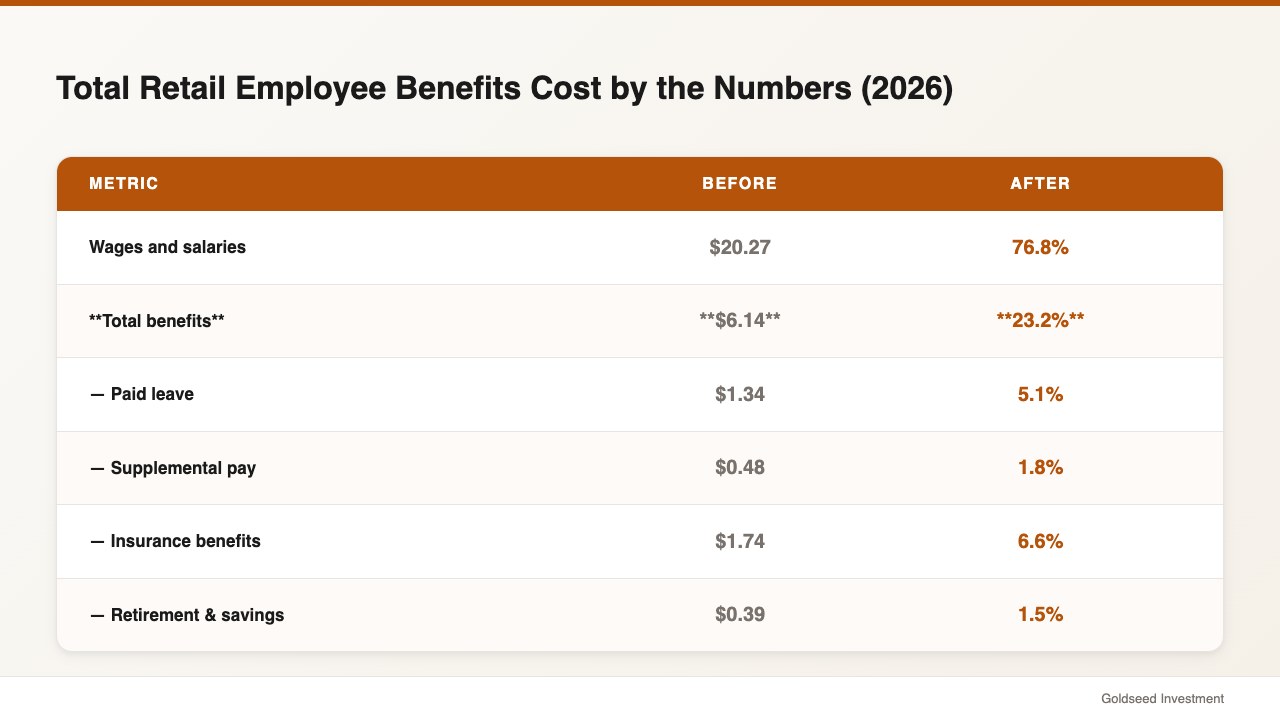

Total Retail Employee Benefits Cost by the Numbers (2026)

The most authoritative source for retail benefits cost data is the Bureau of Labor Statistics Employer Costs for Employee Compensation (ECEC) survey, which tracks compensation by industry quarterly. The December 2025 release provides the clearest current picture of what retail employers pay:

| Component | $/Hour | % of Total Compensation |

|---|---|---|

| Wages and salaries | $20.27 | 76.8% |

| Total benefits | $6.14 | 23.2% |

| — Paid leave | $1.34 | 5.1% |

| — Supplemental pay | $0.48 | 1.8% |

| — Insurance benefits | $1.74 | 6.6% |

| — Retirement & savings | $0.39 | 1.5% |

| — Legally required benefits | $2.19 | 8.3% |

| Total compensation | $26.41 | 100% |

Source: BLS ECEC, December 2025 — Retail Trade Industry

Annualized at 2,080 hours per year, these per-hour figures translate to:

- Total benefits: ~$12,771/year per full-time employee

- Wages: ~$42,162/year

- Total compensation: ~$54,933/year

Consider what this means in practical terms: a retail employer paying a $20/hour base wage is actually spending the equivalent of roughly $26.41/hour in total labor cost — a 32% premium over the stated wage rate. This is the true employee benefits breakdown retail owners must account for in their gross margin and break-even calculations.

These figures are averages across the entire retail trade sector, which includes everything from luxury department stores to discount grocery chains. Your actual benefits cost will vary based on how many full-time versus part-time employees you have, your geographic location (states with higher minimum wages and stronger labor laws tend to have higher benefits costs), and what optional benefits like health insurance and retirement plans you choose to offer.

Health Insurance: The Biggest Benefits Cost

Health insurance consistently represents the largest voluntary benefits cost for retail employers who offer it. Employer-sponsored health insurance typically accounts for 50–60% of total benefits spend, according to BLS data and benefits consulting benchmarks.

For retail employers in 2025–2026, the typical employer cost for health insurance ranges from $8,000 to $14,000 per covered employee per year, depending on plan design, geographic market, workforce demographics, and whether the employer covers single coverage only or extends to family plans. That translates to roughly $3.85 to $6.73 per hour.

The apparent gap between the BLS insurance figure ($1.74/hour) and the health insurance cost range ($8,000–$14,000/year) reflects a critical factor: retail industry average benefits data includes both employers who offer health insurance and those who don’t, which substantially pulls the average down. According to the BLS National Compensation Survey, only about 53% of retail trade workers have access to employer-sponsored medical care benefits, compared to 73% of private industry workers overall. Among part-time retail workers, access rates drop to around 25–30%.

For a retailer who does offer employer-sponsored health insurance to full-time employees, health coverage alone can easily represent $4–$7/hour in benefits cost — nearly matching or exceeding all other benefits categories combined.

Many retail operators manage health insurance costs by limiting eligibility to full-time employees (typically defined as 30+ hours/week), choosing high-deductible health plan options to reduce premiums, or offering a defined employer contribution and letting employees choose from a range of plan options. Sophia Martinez, owner of a four-location specialty grocery chain in Texas, switched to an HDHP with HSA matching in 2024 and reduced her per-employee health insurance cost by approximately 22% while maintaining full-time staff satisfaction.

Paid Leave: Vacation, Sick Days, and Holidays

Paid leave is the benefits category that retail workers and managers think about most day-to-day, and BLS data quantifies exactly what it costs: $1.34 per hour worked in the retail sector, representing 5.1% of total employer costs.

For a full-time employee working 2,080 hours per year, that amounts to approximately $2,787 in paid leave costs annually. This includes four sub-categories:

- Vacation: The largest component of paid leave. Most retail employers offer vacation time on an accrual basis, starting with 5–10 days per year for new employees.

- Sick leave: State and local laws in many jurisdictions (California, New York, Washington, Massachusetts, Oregon, and others) require a minimum number of paid sick days. Common mandates range from 3 to 5 days per year.

- Holiday pay: Retail typically recognizes between 6 and 10 major holidays with paid time off or premium (time-and-a-half) pay for employees who work those days.

- Personal days: Less common in retail than in office environments, but increasingly offered as a recruiting tool to reduce turnover rate.

Compared to the all-industries average, retail paid leave costs run lower — reflecting both lower base wage rates (which paid leave is calculated against) and the higher proportion of part-time employees who often don’t receive paid leave benefits. According to BLS data, only about 66% of retail workers have access to paid vacation, compared to 79% for all private industry workers.

One area worth watching is the growth in state and local paid sick leave mandates. As of 2026, more than 20 states plus dozens of cities require employers to provide paid sick leave — and several new state-level mandates took effect between 2024 and 2026. Retailers operating in multiple states should audit their sick leave compliance by location, as requirements vary significantly.

Legally Required Benefits You Can’t Avoid

A category that often surprises small retailers is “legally required benefits” — payments employers must make regardless of whether they want to offer any benefits at all. BLS data shows these costs average $2.19 per hour in retail, representing 8.3% of total employer costs.

These are among the most predictable benefits costs across retail employers, because the rates are set by law and apply to virtually every employee. The major components are:

Social Security (OASDI): Employers pay 6.2% of each employee’s wages up to the annual wage base ($176,100 in 2026). For an employee earning $30,000/year, that’s $1,860 in annual employer contributions.

Medicare: Employers pay 1.45% of all wages with no cap.

Federal Unemployment Tax (FUTA): 6% on the first $7,000 of each employee’s wages per year, reduced to an effective 0.6% for most employers. Maximum annual cost: $42 per employee.

State Unemployment Insurance (SUTA/SUI): State-set rates that vary by state and employer experience rating. New employers typically pay a higher “new employer rate” that decreases as they build a positive claims history.

Workers’ Compensation Insurance: Required in almost all states, covering medical expenses and lost wages for employees injured on the job. A typical retail classification rate might be $0.50–$2.00 per $100 of payroll.

Together, these mandatory contributions add a floor to your labor cost percentage that you cannot avoid regardless of how lean your optional benefits package is. For a retail employee earning $35,000/year, just Social Security, Medicare, FUTA, and SUTA alone can total $3,000–$4,500 in annual employer cost — a significant addition to working capital planning.

Other Benefits: Retirement, Supplemental Pay, and More

Beyond health insurance, paid leave, and legally required contributions, retail employers incur costs in two additional categories captured in BLS data:

Supplemental pay ($0.48/hour, 1.8% of compensation): This covers overtime pay, premium pay for weekends or holidays, and shift differentials for evening or overnight work. Retail’s extended-hours nature means supplemental pay is a more significant cost driver than in many other industries. Managing overtime carefully — tracking against your OT threshold and using schedule optimization to avoid excess hours — can meaningfully reduce this line.

Retirement and savings ($0.39/hour, 1.5% of compensation): Retail has among the lowest retirement benefit uptake rates of any major industry. The BLS figure reflects that many retail employers — particularly smaller operators — don’t offer a 401(k) match or defined benefit pension. Among retailers who do offer a 401(k), typical employer match rates are 3–5% of employee contributions up to a cap.

The retirement benefits gap is becoming a meaningful recruiting issue. As job seekers in tight labor markets compare total compensation packages, the absence of retirement benefits puts retailers at a disadvantage when competing for stable, long-term employees. Several states have introduced auto-enrollment retirement savings mandates (CalSavers in California, OregonSaves, and similar programs in Illinois and Colorado) that require employers without qualified plans to enroll employees in state-facilitated programs.

David Kim, HR manager for a regional electronics retail chain with 12 locations, notes that after adding a modest 2% 401(k) match in 2024, their 90-day turnover rate dropped by roughly 15% — a cost that more than paid for itself given the average cost of replacing a retail employee.

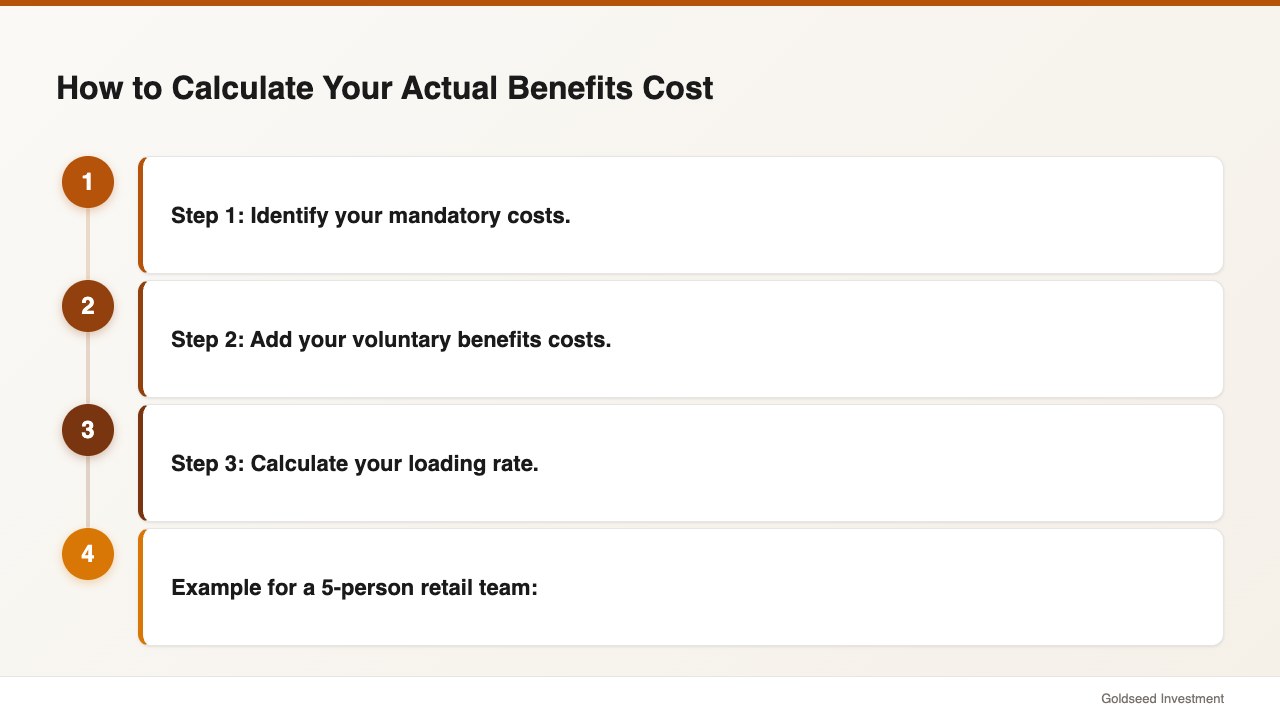

How to Calculate Your Actual Benefits Cost

For retail operators who want to go beyond industry averages and calculate their specific benefits cost, the most practical approach is to use a benefits loading rate — a percentage added on top of wages to estimate total labor cost.

Step 1: Identify your mandatory costs. Take each employee’s gross annual wages and calculate:

- Social Security: wages × 6.2% (up to $176,100)

- Medicare: wages × 1.45%

- FUTA: first $7,000 × 0.6%

- SUTA: taxable wages × your state rate

- Workers’ comp: payroll/100 × your rate per $100

Step 2: Add your voluntary benefits costs. Sum your actual spending on health insurance premiums, paid leave wages, retirement contributions, and any other voluntary programs.

Step 3: Calculate your loading rate. Loading rate = (Total benefits cost ÷ Total gross wages) × 100

Example for a 5-person retail team:

- 5 FTE employees averaging $22/hour

- Annual wages: 5 × $22 × 2,080 = $228,800

- Social Security: $14,186 | Medicare: $3,318 | FUTA + SUTA: ~$1,500

- Workers’ comp (assume $1.20/$100): $2,746

- Paid leave (10 days/employee): ~$8,800

- Health insurance (3 full-time enrolled): ~$30,000

- Total benefits: ~$60,550

- Benefits loading rate: $60,550 ÷ $228,800 = 26.5%

If health insurance isn’t offered, the loading rate drops to roughly 15–18%. With a generous health and retirement package, it can exceed 35%.

For planning purposes, a conservative estimate for a retail operation without health insurance is a 20% benefits loading rate. For retailers offering health coverage and a retirement match, 30–35% is a more realistic planning assumption that protects your gross margin targets.

FAQ: Retail Employee Benefits Cost

What percentage of salary are benefits for retail workers?

Based on BLS data for late 2025, benefits represent approximately 23% of total compensation for retail trade workers — meaning for every dollar of wages, about 30 cents goes toward benefits. This industry-wide average is pulled down by the large number of part-time employees and small retailers who offer minimal benefits. For full-time retail employees at mid-to-large employers who offer health insurance and retirement benefits, the employee benefits cost percentage payroll can reach 30–35%.

Are part-time retail employees entitled to benefits?

Legally required benefits — Social Security, Medicare, unemployment insurance, and workers’ compensation — apply to virtually all employees regardless of hours worked. Voluntary benefits like health insurance, paid vacation, and retirement plans are generally not legally required for part-time workers (defined as fewer than 30 hours/week under the ACA), though some state and local laws require paid sick leave for part-time workers. Most retailers limit voluntary benefits to employees working 30+ hours per week.

How can small retailers manage benefits costs?

Effective strategies include: limiting health insurance eligibility to full-time employees and using a defined contribution approach; choosing high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs) to reduce premiums; using a Professional Employer Organization (PEO) to access pooled benefits pricing that’s typically only available to larger employers; and prioritizing paid leave and retirement benefits, which tend to have higher perceived value relative to their cost.

What’s the minimum legally required benefits in the US?

At minimum, all U.S. employers must pay the employer’s share of Social Security (6.2%), Medicare (1.45%), FUTA, and SUTA taxes, and carry workers’ compensation insurance (required in 49 of 50 states). Employers in states and cities with paid sick leave mandates must provide the required minimum sick days. There is no federal requirement to offer health insurance (for employers under 50 FTEs), paid vacation, retirement plans, or any other voluntary benefits — though state and local requirements continue to expand.

How does retail compare to other industries on how much do benefits cost per employee?

Retail consistently ranks among the lower-benefit industries in the U.S. Private industry workers average $13.58/hour in benefits, compared to retail’s $6.14/hour. Industries like utilities ($22.62/hour), finance ($18.43/hour), and government ($24.11/hour) substantially outpace retail. Retail’s lower figure reflects both lower base wages and the industry’s higher proportion of part-time workers who receive fewer benefits. When benchmarking your retail benefits package cost against published data, use retail-industry-specific figures rather than all-industry averages.

Understanding the true cost of retail employee benefits is the first step toward building a labor budget that doesn’t produce surprises mid-year. Whether you’re hiring your first employee or planning expansion, using BLS retail-specific benchmarks as a baseline — and adjusting upward based on your actual health insurance and leave costs — gives you a defensible, data-backed number to build your gross margin model around.

Sources: BLS ECEC December 2025 | BLS NCS March 2025 | BLS ECEC June 2025 | Selerix Benefits Benchmarks