Convenience stores that implement dual-count procedures and daily over/short tracking reduce unexplained cash discrepancies by 40–60%, according to loss prevention industry data.

Marcus owned two convenience stores in suburban Ohio for six years before he found the pattern. A slow bleed — $50 here, $120 there — had been running for nearly seven weeks before he pulled the over/short report filtered by employee. The same name appeared at the top every week. By then, the total was close to $800. No confrontation had happened. No system had flagged it. He had simply not been looking in the right place.

That’s not unusual. Cash theft at convenience stores tends to surface late — long after the opportunity has repeated itself into a habit.

Why Is Cash Theft So Common at Convenience Stores?

Convenience stores are, structurally, one of the highest-risk environments for cash theft in all of retail.

The average c-store processes between $6,000 and $15,000 in daily cash transactions, according to Convenience Store News industry benchmarks. Unlike a big-box retailer where a single cashier handles a small fraction of daily volume, the convenience store cashier often touches nearly all of it — across a solo shift, with minimal oversight.

The National Retail Federation’s 2023 Retail Security Survey found that employee theft accounts for 28.5% of total retail shrinkage, making it the second-largest driver after external theft. For c-stores specifically, cash larceny tends to rank higher than in other retail formats because of how cash-heavy the business model remains.

Three structural factors compound the risk:

High staff turnover. Convenience store cashier turnover tends to run well above the retail industry average, which means a rotating cast of newer employees who haven’t built loyalty — and who know they may not stay long.

Solo shifts. Many c-stores run single-cashier shifts for 8 or more hours, especially overnight. When there’s no one else watching, the friction against theft drops considerably.

Cash-heavy operations. Despite growing card usage, cash still makes up a large share of c-store transactions, particularly for tobacco, lottery, and under-$10 purchases. Large daily cash volumes create both opportunity and camouflage — small amounts removed regularly tend to look like legitimate discrepancy.

The Association of Certified Fraud Examiners 2024 Report to the Nations found that the median cash larceny loss in retail environments reaches $102,000 — and that most cases go undetected for 12 months or more before discovery.

Understanding why the environment is risky is the starting point. The next step is knowing what to watch for.

What Are the Warning Signs of Employee Cash Theft?

In most cases, cash theft doesn’t announce itself. It tends to appear first as minor, easily explained noise in the data. The warning signs often look like honest mistakes — which is exactly why they get dismissed.

The signals worth tracking:

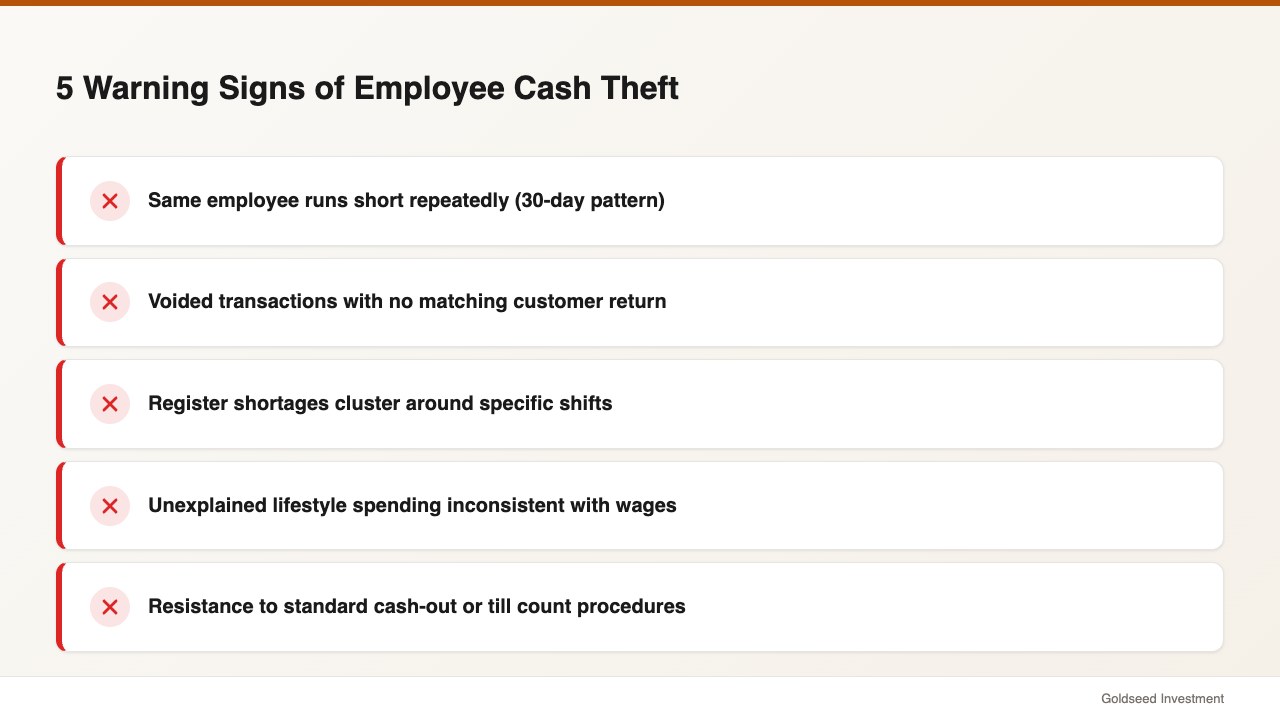

Repeated cash shortages from the same employee. A single $5 short is noise. A $10–$40 short two or three times in a single month, always from the same name, suggests a pattern. Filter your over/short report by employee across a 30–60 day window. The pattern often becomes visible within two weeks.

Voids and no-sale register opens without corresponding customer activity. Exception reporting in most POS systems can flag voids that weren’t followed by a new transaction — or register opens with no sale rung. These are common methods for removing cash while the drawer is legitimately open.

Register shortages that spike during specific shifts. If shortages cluster around a particular time slot rather than spreading across the day, the problem is more likely people than procedure. Compare over/short averages by shift, not just by individual.

Lifestyle inconsistencies. This is harder to track but worth noting: an employee who mentions new purchases, meals out, or other spending that seems inconsistent with their hours can occasionally surface as a pattern worth watching. It’s not evidence — but combined with register data, it changes the calculus.

Resistance to standard cash-out procedures. Employees who consistently push back on counting requirements, rush through till reconciliation, or are uncomfortable when a manager observes the close-out process sometimes have a reason for that discomfort.

One retail operator managing multiple locations described the experience this way: “Before, when numbers didn’t match, I had no way to know if it was theft, a counting error, or a receiving mistake. Now the system tells me statistically whether the discrepancy is random or deliberate.”

This distinction matters. Honest mistakes and theft can produce nearly identical data — the difference is in the pattern, the frequency, and the concentration.

How Can Cash Handling Procedures Prevent Theft?

Most cash theft at convenience stores doesn’t require sophisticated methods. It relies on gaps in process. Close those gaps, and the opportunity shrinks considerably.

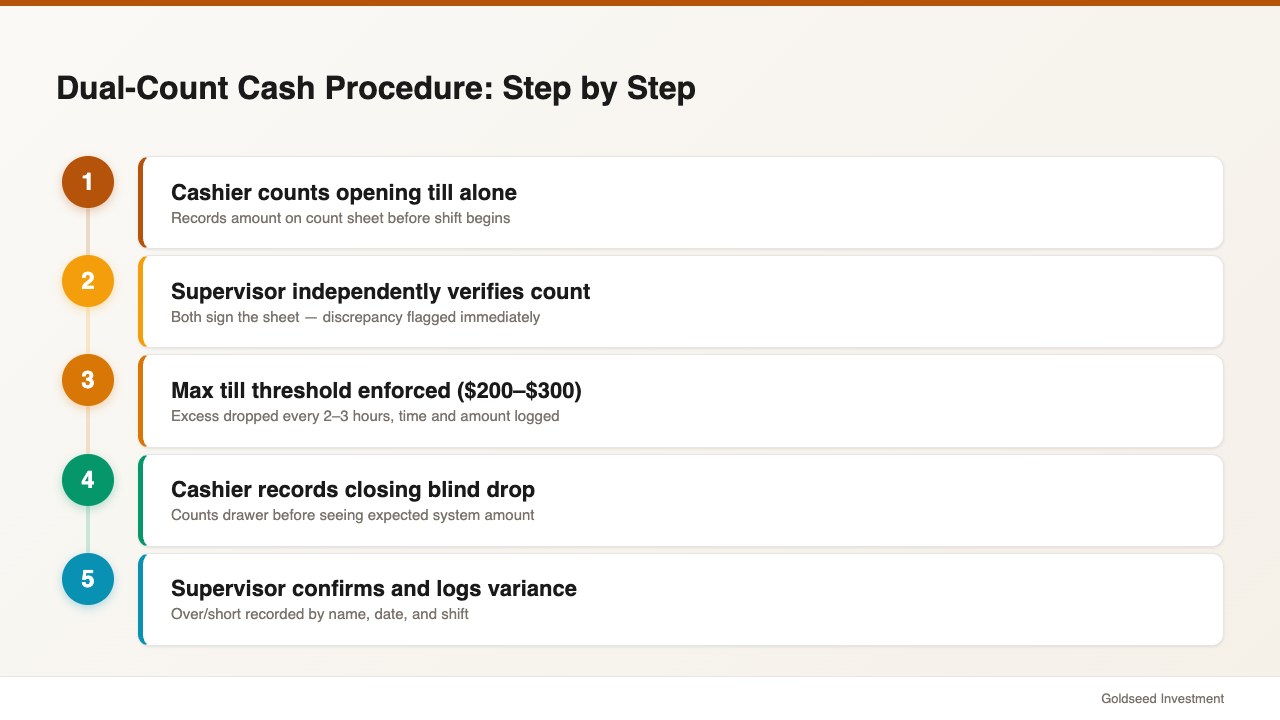

Dual-count drawer procedure. Require that two people count the drawer at the start and end of every shift — one being a manager or shift lead. The cashier counts first, the supervisor verifies. Both sign the count sheet. This alone is one of the most effective deterrents available: it removes the ability for an employee to miscount the opening balance and pocket the difference later. Loss Prevention Magazine data suggests c-stores that implement dual-count procedures see a 40–60% reduction in unexplained cash discrepancies.

Blind drop. Before any manager verification, the closing cashier records their own count of the drawer on a sealed slip — without seeing the expected amount. This prevents the common practice of “working to the number,” where a cashier adjusts their count to match what the system shows rather than what’s actually in the drawer.

Maximum till threshold. Set a rule that the drawer never holds more than a specific amount — commonly $200–$300 for a c-store. Any cash above that threshold goes into a drop safe. This limits the potential loss per incident and gives cashiers less to work with.

Regular cash drops with a log. Every 2–3 hours during peak shifts, excess cash is dropped and the time, amount, and employee name are recorded. This keeps the till manageable and creates a documented chain of custody for all cash movements.

Starting till consistency. The opening till should always be the same amount. Varying the starting balance makes it harder to reconcile accurately and introduces ambiguity that can be exploited.

These procedures don’t require expensive technology. A printed count sheet, a drop log, and consistent enforcement are enough to implement the core controls. For a deeper look at how these processes connect to your store’s overall financial health, see how convenience store financials are structured.

Physical Controls That Reduce Cash Theft Risk

Procedure works best when the physical environment reinforces it. Several physical controls in a c-store can reduce theft risk substantially.

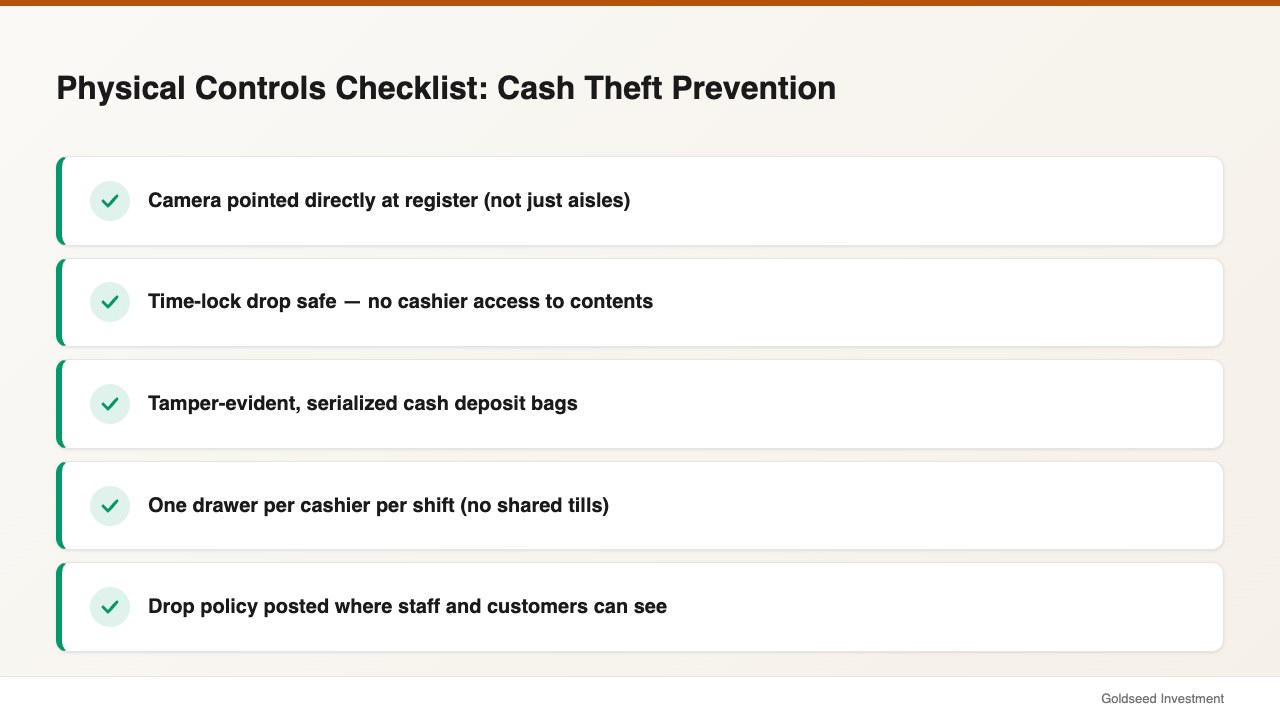

Camera placement over the register, not the aisle. Many c-stores have cameras positioned for general deterrence — pointed at product shelves, entry points, or the beer cooler. For cash theft investigation, the register area is what matters. A camera with a clear view of the register keyboard, the drawer, and the cashier’s hands provides the footage needed to cross-reference transactions against behavior.

Time-lock drop safe with no employee access. A drop safe accepts cash going in but can’t be opened by cashiers. Only managers hold the combination or key card, and opening requires a logged access event. This separates cash storage from cash handling at the operational level.

Tamper-evident deposit bags. All cash leaving the store for deposit should go into serialized, tamper-evident bags. The serial number is recorded at packing and matched at the bank. This closes the window between the store and the deposit.

Single drawer per shift. Each cashier should work from their own assigned drawer for their entire shift — not from a shared till. This makes individual accountability clean and eliminates the ability to attribute shortages to “whoever was here before me.”

Visible drop policy signage. Post the cash drop policy where employees and customers can see it: “Maximum $X in register. Excess cash removed every 2 hours.” This serves two functions — it signals to potential thieves that large amounts won’t accumulate, and it reinforces to honest employees that the procedure is real and monitored.

How Does Technology Help Detect and Deter Cash Theft?

Physical and procedural controls reduce opportunity. Technology reduces the time between an incident and its detection — which, in many theft cases, is the critical variable.

The core technologies worth understanding:

POS exception reporting. Most modern point-of-sale systems can generate exception reports that flag unusual patterns: high void rates, repeated no-sale drawer opens, transactions voided shortly after being rung, and refunds processed without a corresponding return. Reviewing these reports weekly — or setting automatic alerts for threshold breaches — changes how quickly suspicious activity becomes visible.

Over/short tracking by employee. This is the single most useful report for detecting cash theft. A running log of each cashier’s over/short history, filterable by date range, surfaces the statistical outliers. Most honest cashiers fall within a narrow band. An employee consistently running $30–$60 short, particularly compared to others working the same shifts, stands out clearly.

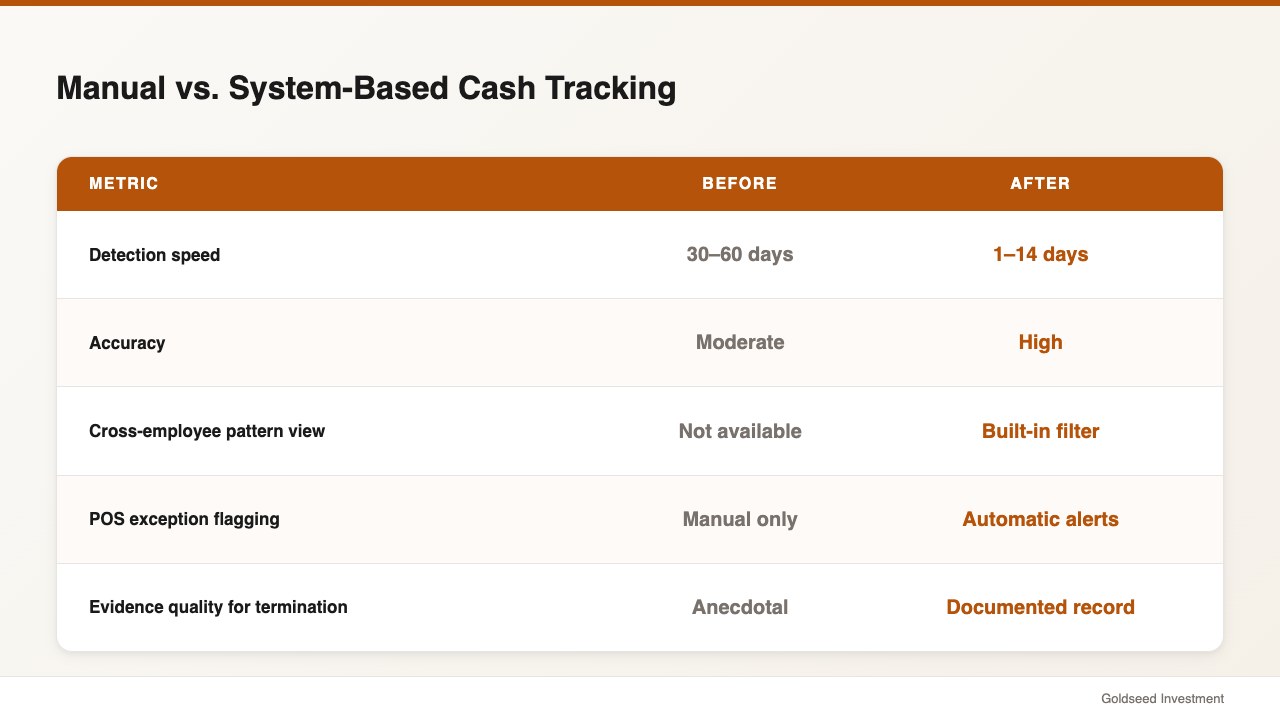

A comparison of what manual tracking versus system-based tracking typically captures:

| Method | Detection Speed | Accuracy | Pattern Visibility |

|---|---|---|---|

| Manual (paper log) | 30–60 days | Moderate | Low — no cross-employee view |

| POS over/short report | 7–14 days | High | Medium — per-employee trend |

| Integrated cash + POS tracking | 1–7 days | Very high | High — cross-reference by shift |

Source: Loss Prevention Magazine, 2024

Video and POS integration. Some surveillance systems allow timestamp synchronization with POS data, so you can pull a transaction — say, a $47 void at 3:14 PM — and jump directly to that timestamp in the footage. Without this integration, cross-referencing requires manual matching, which rarely happens until an investigation is already underway.

Remote dashboard access. Cloud-based reporting from a POS or back-office system allows owners to review daily cash summaries, exception flags, and over/short data from anywhere — without requiring a physical visit to the store. For owners managing two or more locations, this significantly reduces the information delay that lets patterns go unnoticed. This connects to broader questions about what drives profitability across retail store types and how much visibility owners typically have into their numbers.

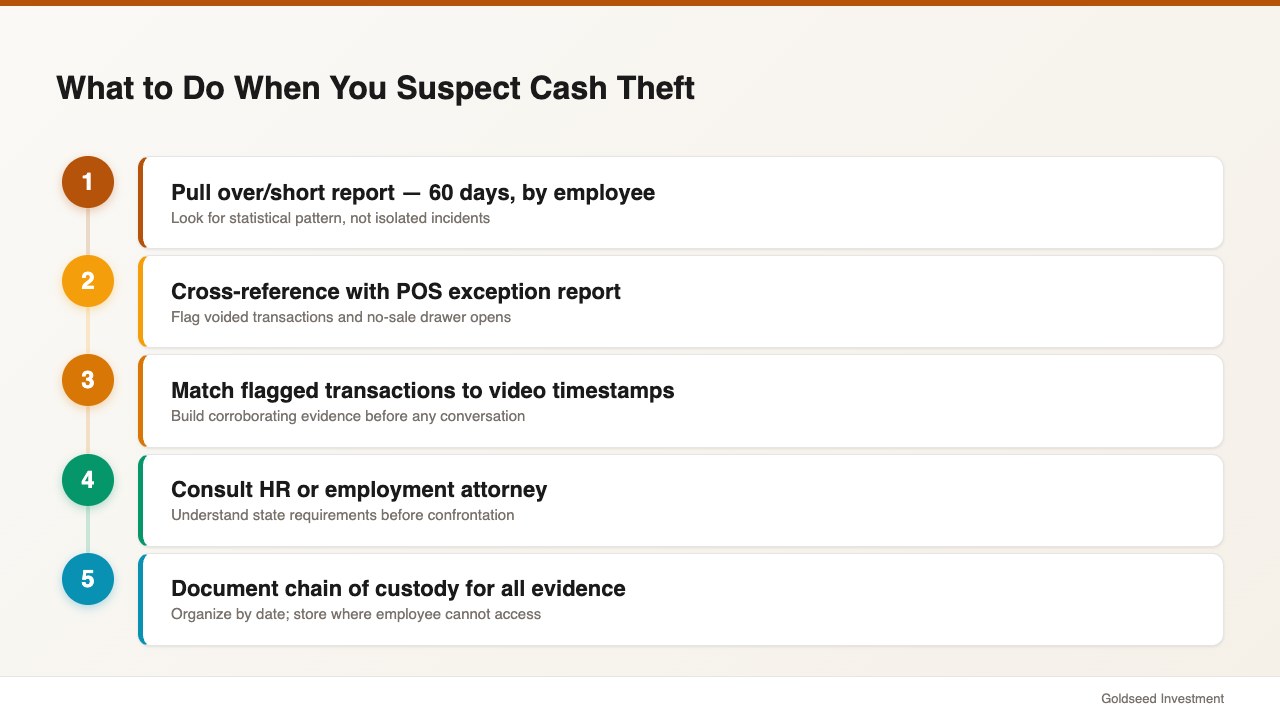

What Should You Do When You Suspect Cash Theft?

When the data starts pointing in a direction, the instinct is often to act quickly. That instinct tends to produce worse outcomes than a measured approach.

Pull the documentation first. Before any conversation, build the factual record. Pull over/short reports for 60 days, filtered by the employee in question. Print exception reports showing voided transactions, no-sale opens, or other anomalies on their shifts. Time-stamp the evidence. The goal is a clear, date-specific pattern — not a collection of impressions.

Cross-reference with video when possible. If your camera system allows it, pull footage for 3–5 of the flagged transactions. Match the timestamp to the behavior. A void at 2:47 PM with no customer visible at the register at that time is a different kind of evidence than a count sheet discrepancy.

Consult before confronting. Employment law around termination, accusations of theft, and evidence requirements varies by state. Before any confrontation, a conversation with an HR professional or employment attorney tends to protect both the investigation and the business. Acting too quickly — or without sufficient documented evidence — sometimes results in wrongful termination exposure that exceeds the original loss.

Document the chain of custody. All evidence gathered — reports, footage, signed count sheets — should be organized with dates and stored somewhere the employee in question cannot access. If the situation proceeds to termination or legal action, this documentation is what allows the case to hold.

Understand what proof is required for your next step. Termination for cause typically requires a different evidentiary threshold than involving law enforcement. Know which outcome you’re building toward before the confrontation, and gather evidence appropriate to that standard.

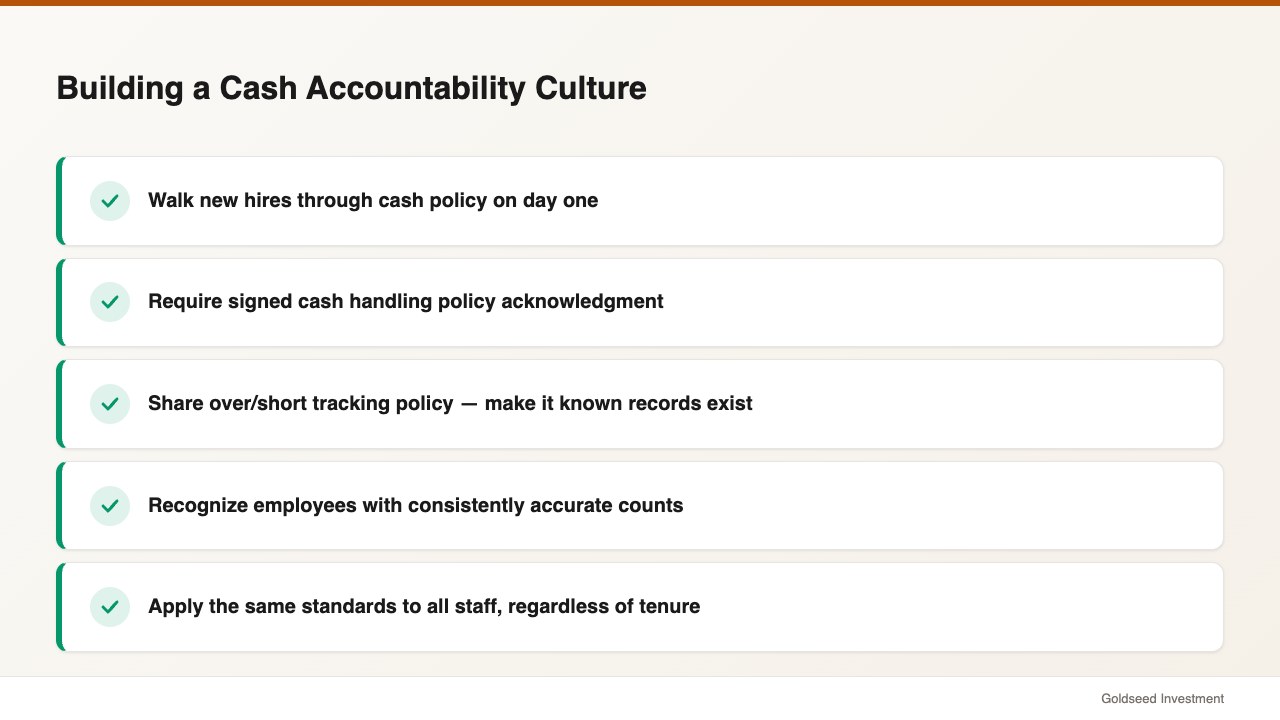

Building a Culture Where Theft Has No Room to Hide

The most effective long-term deterrent isn’t a camera or a procedure. It’s the employee’s knowledge that accountability is ongoing, visible, and applied consistently to everyone.

This is sometimes called a culture of accountability — and in a c-store context, it’s less about culture-building as a concept and more about making sure your tracking systems are visible to the people they track.

Make the over/short record known. Employees who understand that their cash accuracy is tracked over time — not just reviewed after a problem surfaces — behave differently than those who assume each shift stands alone. During onboarding, walk new hires through the cash procedures, the count sheet, and the over/short policy. Make clear that the record exists and that it’s reviewed regularly.

Acknowledge employees with accurate records. A cashier who runs consistently accurate counts over 6 months deserves recognition — even if it’s only a brief comment from a manager. It signals that the tracking system exists in both directions, not just as a punitive mechanism.

Require signed acknowledgment of the cash policy on day one. A signed cash handling policy — one that includes the dual-count requirement, the drop policy, and the consequences for discrepancies — creates a documented baseline. Most employees who later face a theft investigation claim they didn’t understand the rules. A signed document removes that option.

Apply the same standards to everyone. One of the fastest ways to undermine cash accountability is inconsistency. If some employees are held to the count sheet and others aren’t, the procedure becomes a formality rather than a control. Apply the same standards regardless of tenure.

One retail operator who discovered a six-month pattern of manager misconduct at one of their stores later reflected: “I found out six months later that my manager had been letting things slide. I never had a way to know. Now the system knows — and so do I, in real time.”

The shift from detection to deterrence depends on that real-time visibility. When employees know their cash performance is tracked continuously — and that the records are reviewed — the decision to take money changes from a low-risk habit into a much higher-risk calculation.

FAQ

Q: How much cash theft is typical for a convenience store? A: According to the NRF 2023 Retail Security Survey, total shrinkage in retail averages 1.6% of sales. For cash-heavy c-stores, internal theft tends to run higher than the retail average. The ACFE 2024 Report to the Nations found that the median cash larceny loss in retail was $102,000, with most cases going undetected for 12 months or more.

Q: What is the most effective way to prevent cash theft without expensive technology? A: Dual-count drawer procedures — where two people count the till at the start and end of every shift — are consistently cited as the most cost-effective deterrent. Loss prevention data suggests this single procedure reduces unexplained discrepancies by 40–60%. Combined with a signed cash policy and a manual over/short log by employee, these three steps require no technology investment.

Q: Can I fire an employee for cash theft based on over/short records alone? A: Over/short data is supporting evidence, not typically sufficient for termination for cause on its own. Employment attorneys generally recommend corroborating evidence — such as POS exception reports, video footage, or signed acknowledgment of the count — before moving to termination. State-specific employment law also affects what threshold of documentation is required. Consult an HR professional before taking action.

Q: How often should I review over/short reports? A: Weekly reviews are the recommended baseline. Reviewing daily is better if you suspect an active issue. A 30–60 day view filtered by employee is the most useful format for detecting patterns rather than isolated incidents.

Q: What’s the best camera placement for cash theft detection at a convenience store? A: Point at least one camera directly at the register area — with a clear view of the drawer, the keyboard, and the cashier’s hands. Aisle cameras deter shoplifting but rarely capture the register-level behavior relevant to cash theft investigation. If your system supports POS integration with timestamp synchronization, that setup dramatically reduces the time required to investigate flagged transactions.