About 20 percent of new businesses fail in their first year, and the most common reason is not bad ideas — it is underfunded capital reserves and a lease signed before the inventory math was finished.

Priya Anand spent six months scoping a 1,400-square-foot home goods concept in Raleigh, North Carolina. She had a clear vision, a logo, and three vendor relationships. What she did not have, until two weeks before signing the lease, was a working capital model. When she finally built one with a friend who ran a coffee shop, the gap was startling: she was $38,000 short of a real six-month reserve, and her inventory turnover assumption was almost double what the category actually delivered. She caught it in time. Many first-time operators do not.

This guide walks through how to open a retail store from concept to grand opening in twelve concrete steps, with real cost ranges and the math behind each decision. The goal is not to romanticize starting a small retail shop — it is to give you the pre-flight checklist that experienced operators wish they had used.

Why Do So Many First-Time Retail Stores Fail in Year One?

Federal data from the U.S. Bureau of Labor Statistics shows that roughly 20 percent of new businesses close within twelve months, and about 45 percent within five years. In retail specifically, the pattern is consistent across categories. Most first-year failures trace back to three structural mistakes rather than poor product selection.

The first is undercapitalization. A retail store consumes cash through inventory long before sales catch up. Stores that open with less than six months of operating reserve in the bank tend to make survival decisions — marking down healthy stock, cutting payroll mid-week, or skipping vendor payments — that compound into closure.

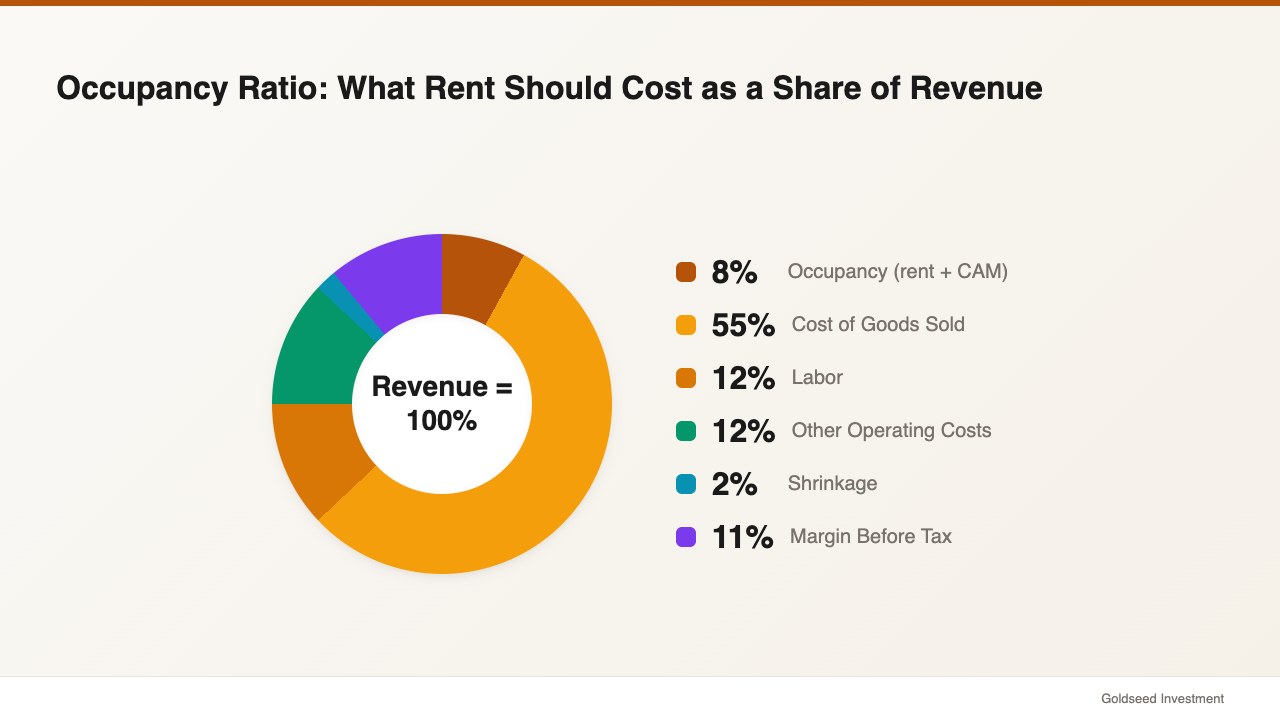

The second is location math. Occupancy ratio, the share of revenue eaten by rent and common-area maintenance, typically should sit between 5 and 10 percent for an independent retailer. Above 12 percent, a positive net margin becomes structurally hard for most formats.

The third is the absence of an inventory-turn plan. A store with 1.5x annual turnover and 40 percent gross margin generates a very different cash flow than a store with 4x turnover at the same margin. Most first-time owners never model this before signing a lease.

A 12-step opening process exists to put those numbers on paper before the bank loan is drawn and the lease is countersigned. It is the cheapest hedge in the entire process.

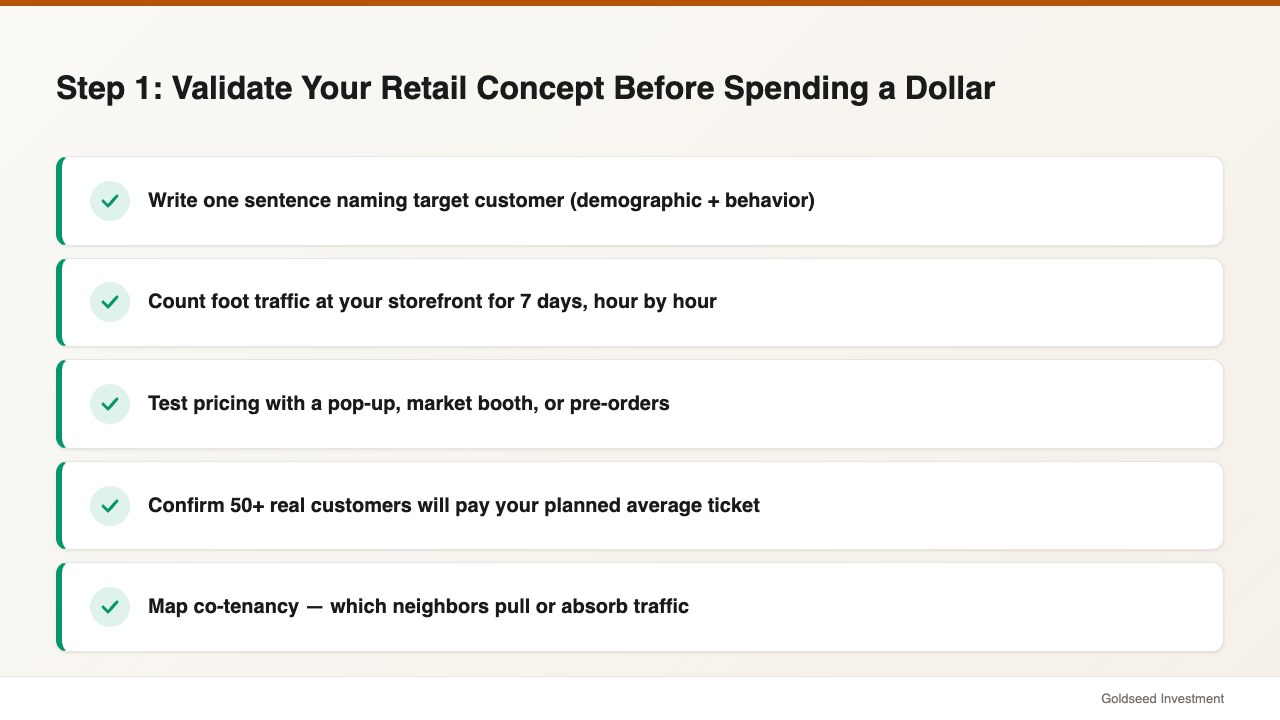

Step 1 — How Do You Validate Your Retail Concept Before Spending a Dollar?

Concept validation is the work that happens before the business plan, and it is where most undercapitalized stores quietly lose their footing. The goal is to confirm three things: a real target customer, a real trade area, and a real willingness to pay.

Start by writing a single sentence that names your target customer in concrete demographic and behavioral terms. “Women aged 28 to 45 who walk this six-block district during weekday lunch hours and currently buy gifts on Etsy” is useful. “Style-conscious shoppers” is not.

Then walk the trade area. Spend seven days, mixing weekday and weekend, counting foot traffic at the precise storefront you are considering. Time-stamp the count by hour. This is the most informative two hours per day you can spend, and it tends to surface co-tenancy patterns — which neighboring stores pull traffic and which absorb it — that no broker report will tell you.

Finally, test pricing assumptions with a pop-up, a market booth, or pre-orders. If you cannot get fifty real customers to pay your planned average ticket before the store exists, the post-opening conversion math suggests caution.

Step 2 — What Goes Into a Retail Business Plan That a Bank Will Actually Read?

A retail business plan that opens lender doors typically contains six sections: executive summary, market analysis, competitive positioning, operations plan, marketing plan, and three-year financial projections. The U.S. Small Business Administration publishes a free template that most SBA-preferred lenders recognize.

The section that often gets undercooked is financial projections. Lenders look for a three-year cash flow model that bakes in shrinkage at 1.5 to 2 percent of revenue, seasonality with at least one negative-cash month, and inventory turn assumptions matched to category benchmarks rather than founder optimism. A plan that shows 6x turnover for a specialty gift shop will not survive due diligence.

Include a sensitivity analysis: what happens if sales are 20 percent below plan, or labor cost ratio runs 4 points above target. Stores that survive the first year often did this exercise on paper before the store opened.

Step 3 — How Much Money Do You Need to Open a Retail Store?

Opening cost ranges depend heavily on format and location, but Forbes Advisor’s retail startup data places typical small retail openings between $50,000 and $250,000. Below that range is usually a kiosk or pop-up; above it suggests either a premium location, a high-inventory category, or significant build-out.

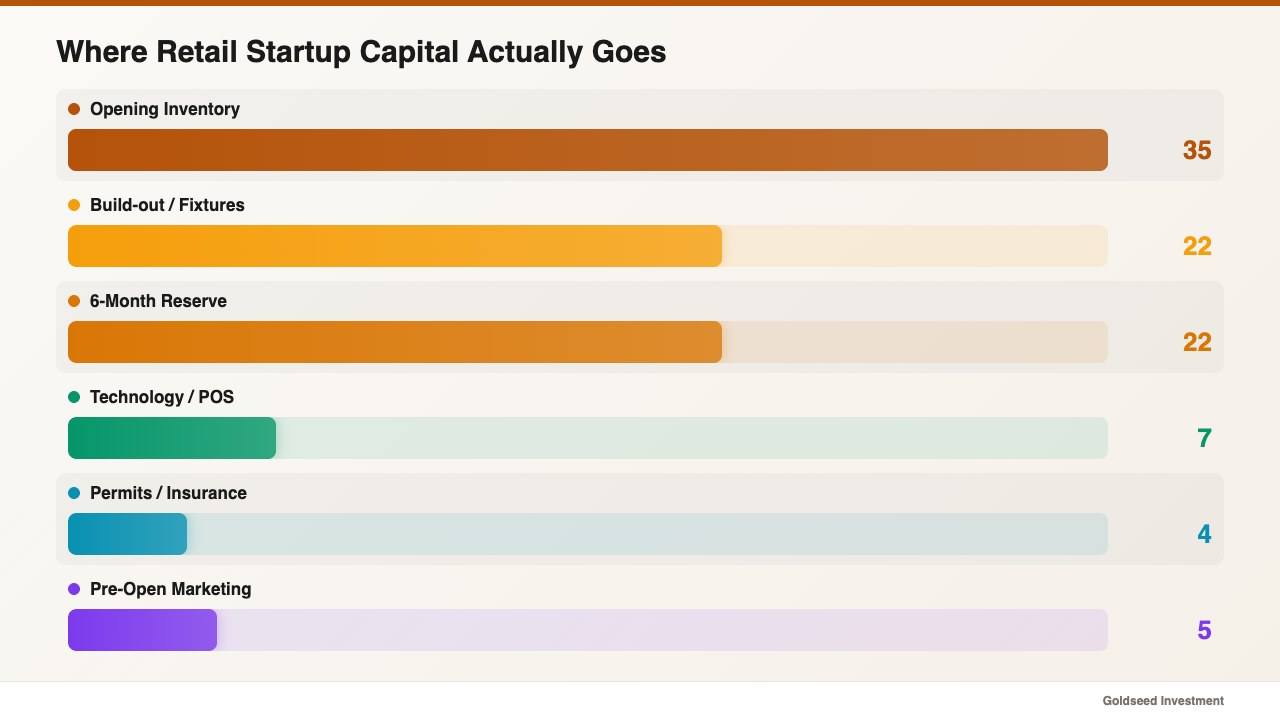

A practical budget breakdown for a first-year independent store:

| Category | Typical Share of Opening Budget |

|---|---|

| Opening Inventory | 30–40% |

| Build-out, Fixtures, Signage | 20–25% |

| Six-month Operating Reserve | 20–25% |

| Technology (POS, network, security) | 5–8% |

| Permits, Legal, Insurance | 3–5% |

| Pre-opening Marketing | 3–5% |

| Working Capital Buffer | 5% |

Source: Forbes Advisor, 2024; NRF Small Business Snapshot, 2025

The single most undersized line item among first-time founders tends to be the operating reserve. Stores that open with six months of fixed costs in reserve survive opening surprises that destroy thinner cash positions. Capital sources include the SBA 7(a) loan program, SBA 504 CDC loans for real estate, vendor net-30 terms, inventory-secured lines of credit, and owner equity. Layering two or three sources usually beats one large loan.

One retail operator who scaled from a single camera shop to a multi-location operation described it bluntly: “Revenue felt real. But the cash wasn’t there when we needed it. The first year is about cash, not sales.”

Step 4 — Should You Form an LLC, S-Corp, or Sole Proprietorship?

Entity selection has tax and liability consequences that compound over time. Three structures cover most first-year retail openings.

A sole proprietorship is the simplest and cheapest to form but offers no liability separation. A slip-and-fall lawsuit reaches the owner’s personal assets. Most retail attorneys advise against it for any storefront business.

An LLC, the most common choice for independent retail, offers liability separation and flexible pass-through taxation. Costs to form range from $100 to $800 depending on state, plus annual filing fees.

An S-Corporation election (which an LLC can adopt) tends to save self-employment tax once the business is profitable enough to pay the owner a reasonable salary plus distributions, generally past $60,000 to $80,000 in annual net income.

Whichever structure you choose, you will also need an Employer Identification Number from the IRS, a state business registration, and a sales tax permit in your operating state. Multi-state online sales add nexus rules and may require permits in additional states.

Step 5 — How Do You Pick a Retail Location That Won’t Bury You in Rent?

Location is the most leveraged decision in opening a retail store. A 200-basis-point increase in occupancy ratio — from 8 percent of revenue to 10 percent — is often the difference between a 4 percent net margin and a 2 percent net margin.

Negotiate the lease around four levers. The first is base rent and the occupancy ratio it implies against your sales forecast. The second is CAM, or common-area maintenance, which can add 15 to 30 percent on top of base rent in mall and lifestyle-center locations. The third is the term and renewal structure; a 3-year initial term with a 3-year option offers more flexibility than a flat 5- or 10-year commitment. The fourth is exclusivity and co-tenancy clauses that protect you from a competing tenant moving into the same property.

Daypart traffic analysis matters as much as total foot traffic. A 1,500-walker hour at 7pm in a restaurant district may convert worse than a 600-walker hour at 11am in a coffee-shop district, depending on your category. Generally, the location that converts well for your specific product mix beats the location with the highest raw traffic.

For a deeper breakdown of the full opening sequence, the retail store opening checklist covers lease, permit, and build-out timing in a single workflow.

Step 6 — What Permits and Licenses Does a New Retail Store Need?

Permitting timelines often surprise first-time owners. Plan for 4 to 12 weeks from application to certificate of occupancy, depending on jurisdiction.

Baseline requirements for most retail stores include a general business license from the city or county, a state sales tax permit, a federal EIN, and a certificate of occupancy from the local building department. Sign permits are commonly required separately and often run on their own 4- to 8-week clock.

ADA accessibility compliance applies to virtually every customer-facing retail space and is typically reviewed at the certificate of occupancy stage. Food handler permits apply if you sell any prepared or pre-packaged food. Liquor licenses, when applicable, run on a much longer clock — often 90 to 180 days, and sometimes longer in states with quota systems.

Calculate your permits parallel-pathed with your build-out, not after it. The number of stores that finish build-out only to wait six weeks on a sign permit is larger than it should be.

Which Technology Stack Should a First-Year Retail Store Actually Run On?

Technology decisions in Year 1 tend to compound for years. Five systems typically need to talk to each other from Day 1: point-of-sale, inventory management, payroll and scheduling, accounting, and customer relationship management.

Modern cloud POS systems generally suit independent retailers better than legacy on-premise hardware because they push data into other systems through APIs. Payment processing fees usually fall between 2.3 and 3.0 percent for card transactions, plus a per-transaction fee. A 0.3-point fee difference on $400,000 in annual card sales is $1,200 per year — meaningful for a thin-margin store.

Equally important, and often overlooked, is the back-office layer that sits between POS and accounting. A store that runs a strong POS but tracks payroll on spreadsheets and inventory on a separate app will spend hours each week reconciling data that should flow automatically. The how to choose a POS system for small business guide walks through the specific feature-by-feature evaluation that experienced operators use before signing a multi-year POS contract.

One operator who managed a multi-location buildout described the trap plainly: “The data was always there. The problem was nobody had time to clean it. By the time anyone figured out a product wasn’t selling, the cash had already been sitting there for months.”

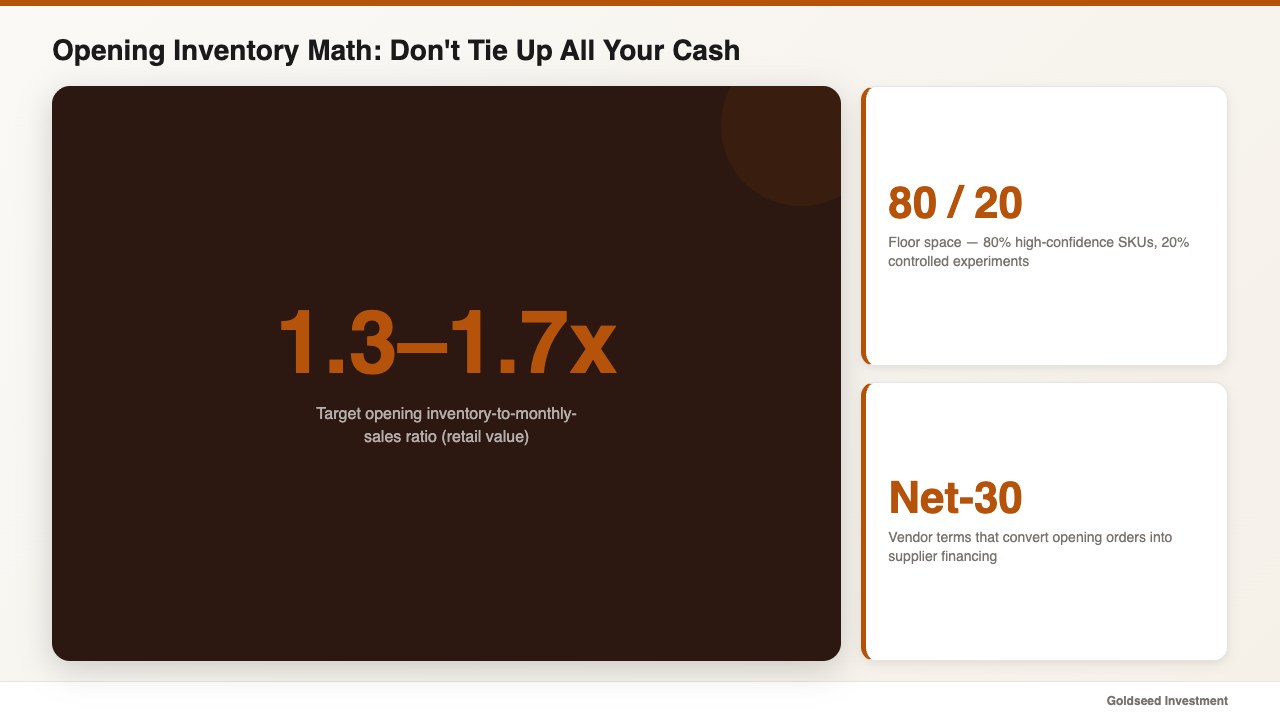

Step 8 — How Do You Plan Opening Inventory Without Tying Up All Your Cash?

Opening inventory is usually the largest single line item in the startup budget, and overbuying is the most common mistake first-time owners make. The target is an opening inventory-to-monthly-sales ratio of roughly 1.3x to 1.7x for most retail formats — meaning if you forecast $40,000 in monthly sales, opening inventory at cost typically lands between $52,000 and $68,000 in retail value, or $26,000 to $40,000 at COGS for a 50 percent gross margin store.

Build your opening assortment around a small number of high-confidence SKUs rather than a wide thin spread. A common rule of thumb: 80 percent of opening floor space goes to products you have firm demand evidence for, and 20 percent goes to controlled experiments.

Negotiate vendor terms before you place opening orders. Net-30 terms convert a portion of your opening inventory into supplier financing. Consignment arrangements, where they exist, push that further. Minimum order quantities tend to be negotiable for first orders, especially with smaller vendors who want shelf placement.

Set reorder points using basic standard deviation logic rather than gut feel. A product that sells 40 units per month with a standard deviation of 10 units needs a different reorder point than a product that sells 40 units per month with a standard deviation of 25 units, even though the average is identical. Reorder math, done once per category, prevents both stockouts and dead inventory.

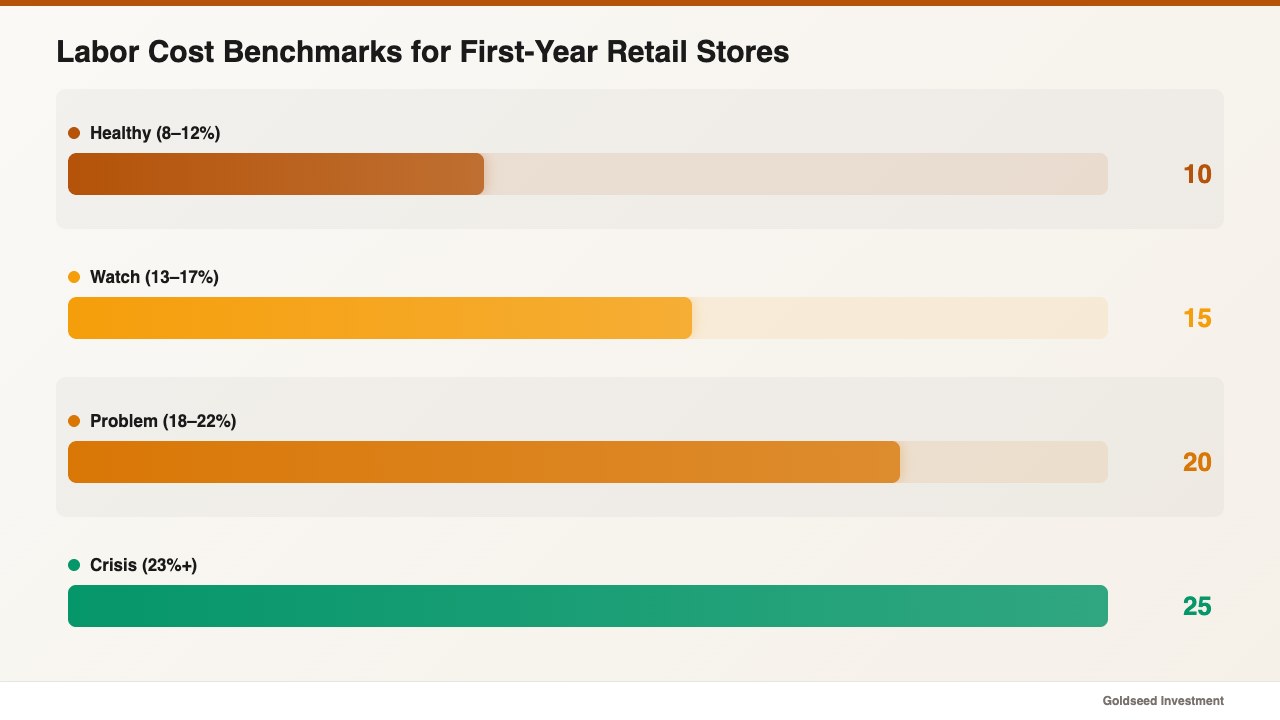

Step 9 — How Many Employees Do You Need on Opening Day, and What Should You Pay Them?

Labor cost ratio is the second-biggest controllable expense after COGS. Stores that run labor at 8 to 12 percent of revenue tend to be sustainable; stores running above 18 percent generally have a scheduling, overtime threshold, or turnover rate problem.

The typical Year-1 setup for an independent retail store is the owner-operator plus two part-time hires, scaling to three or four part-timers once weekly sales exceed roughly $12,000. Predictive scheduling laws now apply in jurisdictions including Oregon, Seattle, New York City, San Francisco, Chicago, and Philadelphia, and they affect how far in advance schedules must be posted and the penalties for last-minute changes.

Pay benchmarks from the BLS Occupational Employment Statistics give a reasonable baseline by metro area. Pay near the median for your local market, not the minimum, if you want to keep turnover rate low — replacing a retail associate typically costs 16 to 20 percent of annual wages once recruiting, training, and lost productivity are tallied.

Step 10 — What’s the Most Cost-Effective Way to Market a Brand-New Retail Store?

Pre-opening marketing spend often gets allocated poorly. The high-ROI moves usually do not require much money.

Set up your Google Business Profile six to eight weeks before opening with photos, hours, and a category that matches search intent. Local SEO basics — consistent name, address, and phone across directories — tend to drive more first-month walk-in traffic than paid ads at this stage.

Run a soft opening for one to two weeks before the announced grand opening. Invite friends, family, neighborhood businesses, and your soft-opening punch list will surface point-of-sale problems, lighting issues, and product flow bottlenecks before paying customers experience them.

Build an owned email list from the soft opening forward. Email tends to outperform paid social by a wide margin for retail repeat-purchase economics. Avoid expensive paid media in Month 1 — your conversion data is too thin to spend efficiently.

Step 11 — How Should You Set Up Your Store Layout, Signage, and First Hours of Operation?

Layout decisions affect conversion rate, basket size, and shrinkage. Place high-margin, high-impulse merchandise at the power wall — typically the wall directly across from the entrance — and leave a decompression zone of roughly 5 to 10 feet just inside the door so customers can adjust before encountering merchandise.

Plan sight lines from the register to the back wall. Visibility reduces loss prevention issues and improves the customer experience.

Hours of operation are worth testing rather than guessing. A common pattern: open the first two weeks with longer hours (say, 9am to 8pm), track sales by hour and conversion rate, and then trim the underperforming dayparts within 30 days. Many independent retailers eventually settle on shorter hours than they originally planned, and the labor savings tend to fund a marketing budget that was missing on opening day.

Build opening and closing checklists before Week 1. Daily cash reconciliation, opening float counts, end-of-day deposit, and a basic markdown protocol should be written down before they become urgent.

Step 12 — What Should You Track in Your First 90 Days?

The first 90 days are the highest-information period in the store’s life. Track daily sales, transaction count, average basket size, and conversion rate from Day 1.

Weekly, review gross margin by category, shrinkage indicators, labor cost ratio, and inventory aging. Monthly, build a basic P&L against the plan you wrote during Step 2, compare actual cash position to projected cash position, and note variance.

The variance, not the absolute number, is what matters most. A store that planned for $35,000 in Month 1 sales and delivered $32,000 with a 6 percent labor cost overrun is in a different situation than a store that delivered the same $32,000 with labor on target. The first signals a sales-side adjustment; the second signals operational discipline.

This isn’t a knowledge problem — it’s a tools problem. Most first-year owners face this not because they’re inattentive, but because the data pipeline was never designed to make this kind of weekly review easy. For first-year retailers, the best POS system for small business comparison is a reasonable starting point for evaluating which platforms surface these metrics natively versus requiring spreadsheet exports.

Common Mistakes That Sink First-Year Retail Stores

A short list of the patterns that recur across closed stores. Underestimating the operating reserve. Signing a lease before modeling occupancy ratio against realistic sales. Hiring before the scheduling and payroll systems are in place. Ignoring shrinkage in Month 1 — even though shrinkage trends often appear in the first 30 days. Marketing spend that front-loads paid social before owned channels are built. Buying opening inventory broad instead of deep, then watching aged stock crowd out faster-moving products by Month 4.

Each of these is recoverable in Year 1 if caught early. The 12-step framework is built to surface them in writing before opening day, when fixing them is still cheap.

FAQ

Q: How long does it take to open a retail store from idea to grand opening? A: Roughly 6 to 12 months for most independent retail openings — about 8 to 10 weeks for concept validation and business plan, 12 to 20 weeks for lease negotiation and build-out, and 4 to 8 weeks for permits running in parallel. Faster than 6 months usually signals skipped due diligence; longer than 12 months often signals capital or location stalling.

Q: How much profit does a small retail store make in Year 1? A: Most independent retailers post a small loss or breakeven result in Year 1, with profitability appearing in Year 2 or Year 3. Industry data from the NYU Stern margin database shows average retail net profit margin lands near 3 percent overall, with category ranges from 1.6 percent in grocery to over 20 percent in specialty and luxury segments. A Year-1 store that approaches 0 to 2 percent net margin is usually on a healthy trajectory.

Q: Do you really need a business plan to open a retail store? A: If you are using outside capital — bank loan, SBA loan, investor money, or vendor net-terms beyond opening orders — a written plan is non-negotiable because the lender or vendor will ask. Even with self-funding, a 10- to 15-page plan that includes a three-year cash flow tends to surface inventory turn and labor cost ratio assumptions that founders otherwise leave unexamined.

Q: What’s the single biggest mistake first-time retail owners make? A: Underestimating working capital. Stores that open with less than six months of operating reserve in the bank typically face survival-mode decisions — markdown pressure, late vendor payments, or cut hours — that compound. The capital math, done before lease signing, is often the difference between Year-2 survival and Year-1 closure.